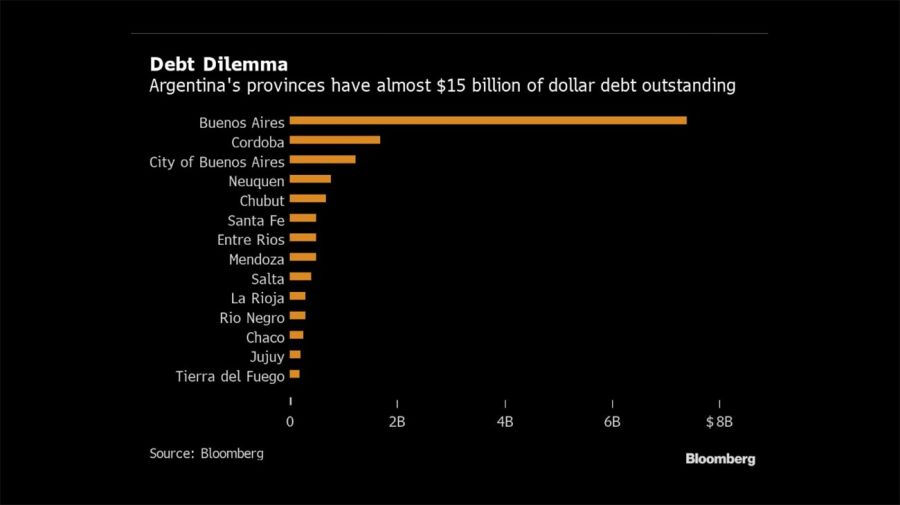

A US$15-billion pile of provincial bonds is lurking below the surface of Argentina’s already imposing sovereign debt load, setting the latest fiscal fiasco apart from any in the country’s history and threatening to saddle foreign investors with even more losses.

The nation’s provinces were among the most prolific issuers when international capital markets reopened to Argentina following business-friendly President Mauricio Macri’s election in 2015. By offering interest rates in excess of nine percent, they were able to lure yield-hungry investors to little known and sparsely populated corners of the country – places like frigid Tierra del Fuego in the extreme south and desert-like Jujuy in the north.

Now money managers are racing to dump the debt amid concerns that local governments will use a potential sovereign restructuring to lessen their own increasingly burdensome debt loads. The fact that many provinces are almost wholly reliant on disbursements from the federal government for the dollars needed to make interest payments only further increases the risk to creditors.

“We got involved in these less financially robust provinces because our thesis was that, at the end of the day, they were getting a lot of transfers from the federal government,” said Ian McCall, who oversees US$190 million in emerging-market assets at First Geneva Capital Partners and has already sold the bulk of his provincial bond holdings. The idea was “Argentina won’t default under Macri, and the provinces won’t default because they will remain assisted by the federal government.”

That thesis was blown up last week when the government announced it would postpone payments on short-term local notes as part of a plan to 'reprofile' more than US$100 billion of debt, a move S&P Global Ratings considered a selective default. The country’s bonds plunged, with many now trading below half their face value.

Reputation

While Argentina is reassuring money managers that efforts to extend US$50 billion of longer-term international debt will be voluntary, the dire fiscal backdrop, the country’s reputation as a serial defaulter and the leftist tack of the likely incoming administration have many wagering it’s just a matter of time before payments on those securities are halted as well. In 2001, Argentina reneged on US$95 billion of bond obligations, then the largest default in history.

Though the sovereign’s debt load isn’t quite as onerous as it was back then, the burden on the provinces is significantly larger. The amount of provincial dollar bonds outstanding is almost double what it was in 2001, according to Fitch Ratings analyst Natalia Etienne, threatening to further upend the nation’s fragile financial state and spark a flurry of creditor negotiations.

While there are neither cross-default clauses nor explicit federal guarantees on provincial bonds, some issuers will have little choice but to follow the sovereign in a default scenario, according to Edward Glossop, an economist at Capital Economics in London.

“After all, their debts are also mostly in foreign currencies, the local-currency value of which has risen sharply as a result of the collapse in the peso,” Glossop said. “Many provinces do not have large dollar revenue streams other than the federal government.”

Among the most beaten-down securities are those of Chaco, La Rioja and Río Negro, which are already trading at less than 50 cents on the dollar.

But perhaps no province stirs more concern than Buenos Aires. With about half of all provincial debt outstanding, it’s seen by many strategists as among the most likely to default should the federal government, given its significant foreign-currency obligations and weaker credit metrics.

The fact that Axel Kicillof – who led Argentina’s last technical default in 2014 and is aligned with the likely incoming administration – appears set to become governor also boosts the odds of a restructuring, according to Delphine Arrighi, a London-based money manager at Merian Global Investors.

None of the four provinces responded to messages seeking comment.

Staying solvent

Of course, not all provinces will fall victim to a sovereign default. Investors say those with access to dollars, such as energy-rich Neuquén, and ones on sounder fiscal footing, such as Coódoba, are safer bets. Most also say notes issued by the city of Buenos Aires – which didn’t default on its obligations in 2001 – are likely to continue paying.

Cordoba has already started to cut its capital expenditure plan in order to preserve the funds necessary to repay its debts in full, according to a government official aware of the plan who asked not to be named because he’s not authorized to speak publicly.

Neuquén – home to the Vaca Muerta shale formation – has the roughly US$100 million needed to service its obligations in the coming year and won’t seek any kind of reprofiling, the provincial economic ministry press department said in an email response to questions.

“What I have been trying to tell global investors is that there is a history of provinces not being dragged down by the sovereign in default situations,” said Daniel Marx, a former finance secretary who now runs Buenos Aires-based consulting firm Quantum Finanzas.

related news

by Aline Oyamada & Pablo González

Comments