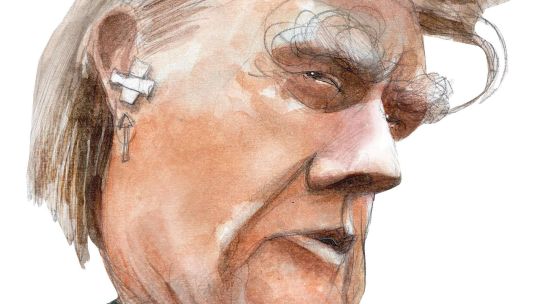

Bahamas Attorney General Ryan Pinder is at the forefront of the Global South’s pushback against worldwide tax policies it sees as “inequitable” and “unfairly applied.” The rules, he argues, are set by the developed world unilaterally, without input from nations like his own.

“We are not belligerent and we're not rude. But we are loud and reasoned in our approach,” he explains during an interview at a hotel in Buenos Aires.

Pinder, 50, serves as Minister of Legal Affairs and Attorney General for the Bahamas, but he is also part of a United Nations committee developing the framework for an international tax convention. An agreement, he argues, would help the Global South adopt policies that would strengthen development.

In a speech in Buenos Aires last week, Pinder highlighted Tax Justice Network reports revealing that Organisation for Economic Co-operation and Development (OECD) “member countries and their dependent territories are consistently responsible for approximately 70 percent of global cross-border corporate profit shifting and tax evasion, and approximately 90 percent of all taxes lost due to offshore evasion by high-net-worth individuals.”

With OECD nations accounting for 78% of worldwide tax losses, the Bahamian asks if “the heavy focus on regions in the Global South is truly justified, or are we looking at hypocrisy and double standards?”

What brings you to Buenos Aires, and what is it that you are working on currently?

I was pleased to come and lead off the conference Society of Trust and Estate Practitioners (STEP) LATAM conference. STEP is a global institution in the financial services industry with thousands of members […]

[Currently], I have a seat on the Ad Hoc Committee at the United Nations [Ad Hoc Committee to Draft Terms of Reference for a United Nations Framework Convention on International Tax Cooperation], where we just finished negotiating the terms of reference for an international tax convention at the UN. I'll sit on the negotiating committee for the actual drafting of the convention over the next three years. We have a firm belief that the appropriate place for tax reform, especially for developing countries [in the Global South] like the Bahamas or Argentina, is the United Nations.

Domestically, I'm the Attorney General and advisor to both the Government and Prime Minister [Philip Davis]. I hold a significant portfolio, almost everything that comes to the country, comes to my desk, because everything has a legal impact.

What are some of your responsibilities on the [UN] committee?

I represent the Bahamas. We're very active in ensuring that the framework of the convention is suitable for small island developing states. I also represent the Caribbean region, CARICOM, on the Bureau, which is a subcommittee of the actual ad hoc committee. The Bureau had responsibility for all of the organisational elements in terms of reference, setting out the priorities and really being kind of a day-to-day negotiating arm for the convention. We are part of GRULAC, which is the Caribbean and Latin America. So we sat there alongside our Latin American colleagues to make sure that our interests were preserved.

Can you give a brief context as to why a committee like this needs to be formed?

The longstanding position of countries like the Bahamas and generally the Global South is that tax policy being [set] in the OECD is inequitable, and it’s unfairly applied. When policy and regulation is developed, it develops without the input from countries in the Global South, because the OECD is an exclusive membership organisation primarily of the developed world.

It's firmly our belief that the forum for something as important as global tax reform should be the United Nations, where every country has equal vote, equal standing, has an ability to provide the input and direction of where global tax policy should go …

That was the motivation for Resolution 78/230, [which] was sponsored by the African countries but supported by the Global South, to draft comprehensive framework convention on tax policy and at the United Nations.

You touched on global tax reform. What does cooperation look like in that regard?

From a country cooperation point of view, as we develop ideas and a direction for the convention itself in the terms of reference, which is what we've just concluded, certainly there's a division between countries and the goals of the developing world versus the Global North.

You would note in my speech I made the point that not a single OECD country voted in favour of the resolution and not a single OECD country voted in favour of the terms of reference. So from a country cooperation point of view, there's clear divergence.

From the actual direction and tax of what we want to see the convention be, certainly no country supports illicit financial flows and tax evasion. So I think an embedded process is a global tax convention that has to address illicit financial flows, has to address tax evasion and those aspects.

But the interests of the Global South goes further than that. For example, as a small island developing state you are very aggressive in linking environmental concerns to tax policy […] Many Latin American countries took the position that they wanted to see a high net worth wealth tax addressed within the convention. Specifically Brazil, supported by Argentina, took that position, as well as Colombia and a couple other Latin American countries …

The Global South was also very concerned about human rights violations and how do you connect human rights policy and taxation together as well …

One element I think is very important is it's now going to address dispute resolution.

So if two countries have a differing opinion on how taxation should work or how a transaction should be taxed or regime put in place, there's not going to be a dispute resolution mechanism.

Countries like the Bahamas and others have fallen victim to unilateral and arbitrary blacklisting by OECD member countries by the EU when they disagree on tax policy with us. That has significant adverse effects for these countries.

What is Argentina's stance in the committee and its goals?

Argentina was an active participant in the committee. Latin America was very unified in their approach. Argentina was very vocal in support of the Global South. So we're grateful for Argentina's voice at the table.

Has Milei pushed for a withdrawal from such global tax reforms?

No, I don't think there's been a withdrawal at all. The Argentine mission in New York has led the charge on that and they have been vocal at the table. I don't think that Milei has, through his policy, caused Argentina to not be supportive.

I think what happens sometimes is [LATAM countries] abstain in solidarity. For example, Mexico and Chile are OECD members. They had a difficult position because they wanted to support the agenda of the Global South, but they were members of the organisation itself. I think the choice was to abstain for global geopolitical purposes. But when it comes down to it, they are supportive and they're unified with the position of the board of directors.

How can this benefit Argentina? What's in it for Argentina?

Clarity on taxing rights for cross-border transactions. Argentina has a very strong agricultural industry that is an export industry. You want to ensure that there are tax revenues from that industry in Argentina. Also, ensuring that there's a proper regime to protect against illicit financial flows … [It would also benefit Argentina] as tax policy and different components evolve. For example, now we're talking about taxation in the digital world. Where would Amazon be taxed? How does a country like Argentina ensure that the transactions and the profits made in its jurisdiction in the digital space get taxed, and the revenues come to the country?

The Bahamas has a reputation for being a tax haven. What's the motivation for this convention now?

We're a low-tax jurisdiction. We have a belief that tax competition is viable. It's an important component of where we are in the world, and how we set up our economic framework. We choose that because that helps us attract inbound investment and economic development and ultimately employment and future for our people. We don't shy away from that.

We are upfront in the fight against illicit financial flows and financial crimes. We don't advocate for that. I think that's an important aspect. We fought hard in this context to ensure that issues of national importance are connected to global tax policy. So you'll see in the terms of reference the connection between environmental concerns and tax policy is a firm commitment. That's an important thing for the Bahamas who, day by day, as the sea water rises, we lose our land mass, we lose economic opportunity […]

You look around the world, and despite what countries say, they believe in tax competition as well. There's an example that was given [at the STEP conference]. Uruguay has a tax holiday for wealthy people. You have Argentines who may be living in Uruguay because the taxes are lower. Well, you know what that is? That's tax competition. So the question is, what is Argentina doing now in a world of tax competition? How do you either track those people back? Or how do you attract other industries through tax competition?

Those are things that I think countries are doing in the national interest. And I don't see a problem with that.

How do you foresee OECD members trying to push back against your efforts?

We certainly anticipate that they will try to disrupt progress in the negotiations with the conventions. They've taken a firm position all along: the Global North believes that decisions around tax policy should be done on a consensus basis. Our position is that we don't trust them. We think that's just them trying to put a veto right within the framework of how decisions are made related to the convention. Our belief is that decisions should be made on a majority basis, even in certain instances on a super majority basis. A consensus basis really is an attempt to stall or derail the efforts in the convention.

We've been put on notice that the Global North is still going to push that issue [...] I don't have any confidence that we're going to be all at a table in agreement. But that's OK. As long as we in the Global South maintain what we're trying to accomplish, and we do it collectively, we ensure that policy is administered fairly and not arbitrarily. The Global South has numbers. So long as it sticks together and shares the common belief of what we want out of it, we will get it.

M: What's the process going to look like going forward?

Well, it's going to be long. Three years is a long time to get to the end. … I look forward to early in 2025, starting the negotiation sessions, putting pen to paper and drafting what the convention framework would look like.

We look forward to having an aggressive position and maintaining our aggressiveness at the table as a country. We look forward to working with our colleagues in the Global South on unified positions [...]

We are not belligerent and we're not rude, but we are loud, we are reasoned in our approach, we do our research, and we think that we have a lot to offer.

Is the ultimate goal to have a permanently established committee?

From a governance point of view of the convention, we envision a conference of the parties being established. That is a full-time governance mechanism on how the convention should operate, with annual meetings where tax policy is discussed and developed [...]

Ten, 15 years ago, you wouldn't think that you need a framework for taxing the digital economy. Today, it's natural, as you think about the intricacies of that. So as the economic world changes, you're going to have tax policy changing with it. So you do need a governance structure or a conference of the parties to be able to guide that year and year.

Do domestic challenges sometimes clash or correlate with what you work on at the UN?

Absolutely. Every country has a certain cultural identity. Sometimes that cultural identity isn't the equivalent of the global identity or what the United Nations is pushing as an important topic. I think that kind of drove Milei’s contribution at the United Nations, where he may see cultural identity of Argentina being on a different track than he sees the agenda setting at the United Nations. All countries may be that one way or the other.

Comments