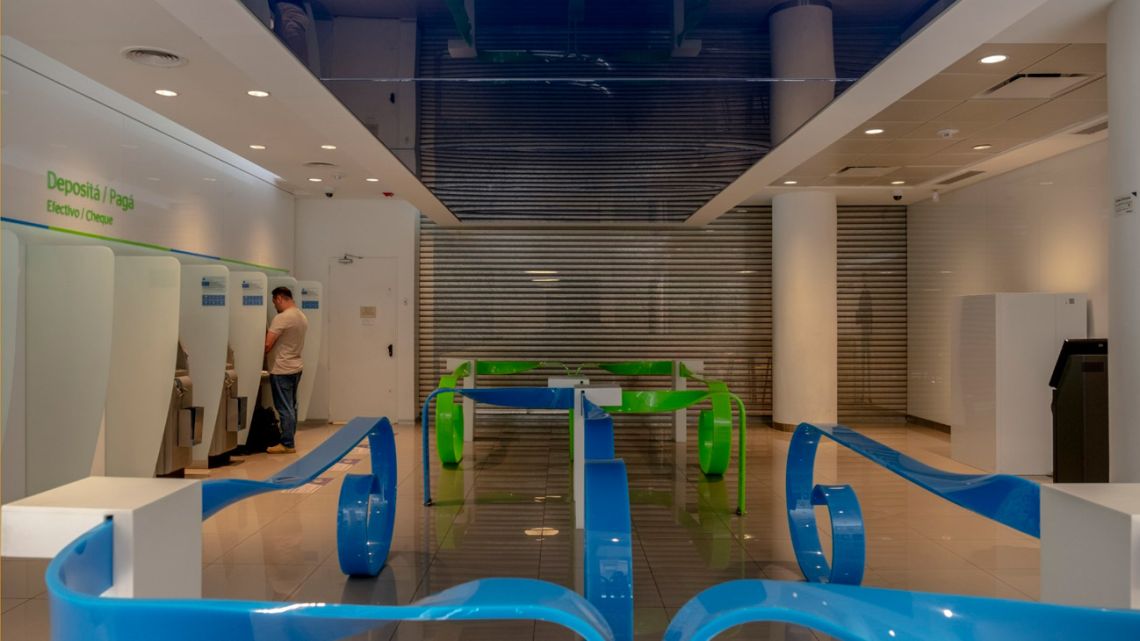

On a weekday afternoon in Buenos Aires, a guard stands watch outside an empty bank. It’s not just devoid of customers: Though the lights are on and Banco Santander’s signature red-and-white decor remains, there isn’t a single employee inside.

Ghost branches like this one — no longer serving clients who require anything beyond an ATM, but not technically closed — have become a common sight in Argentina. As customers increasingly do their banking via smartphone apps and online, Santander and Argentine rivals including BBVA Argentina, Grupo Financiero Galicia and Grupo Supervielle, like their global peers, are pushing to close physical locations. But regulators won’t let them.

The problem, as told by Central Bank chief Miguel Pesce to industry representatives, is the country’s powerful unions. Pesce has said that authorising permanent branch shutdowns is difficult because he’s under pressure from labour leaders worried about job losses, according to two people with direct knowledge of the discussions. A spokesman for the Central Bank said unions don’t sway its decisions to close branches or leave them open.

It’s an expensive dilemma for Argentina’s banks, already hammered by soaring inflation and caps on lending rates. The banks argue that their aim isn’t to cut costs by eliminating jobs, saying many employees who worked at the now-empty branches are being reassigned to other locations.

But between leases and other expenses, one industry official estimates that each ghost branch costs about US$500,000 annually to maintain, depending on size. If it weren’t for the regulatory obstacles, executives say, more than a quarter of locations would shut — representing some US$375 million a year in savings.

The phenomenon is putting the country’s banks at a disadvantage to Latin American peers. Just three branches closed in Argentina last year through August, according to Central Bank data — less than 0.1 percent of those operating a year earlier. Chile shut 8.3 percent of its branches over the same period, while Brazil closed 2.2 percent.

In Argentina, “banks’ revenues fell in these last three years, while the operating structure stayed the same,” said Paula La Greca, senior corporate research analyst at brokerage TPCG, which hasn’t recommended Argentine bank stocks for two years. “Union pressure prevents them from cutting jobs and the central bank does not authorise branch closures.”

In Buenos Aires alone, there are more than 100 ghost banks, executives estimate. Many Argentina banks are forced to renew leases they had planned to end because of the Central Bank’s refusal to let them close the branches, said one industry official.

Spokespeople for Santander, Supervielle and representatives of Argentine banking industry groups ABA and Adeba declined to comment. A spokesman for Grupo Financiero Galicia said that while the bank doesn’t have vacant branches, some of its locations in downtown Buenos Aires have had few customers.

Labour leaders argue that reassigning employees to busier branches is not enough. Technology is transforming the industry, reducing the need for tellers and other traditional roles. The number of employees in private banks fell 1.6 percent in the first six months of 2022, according to central bank data.

“We ask the Central Bank not to indiscriminately authorise branch closures,” said Claudio Bustelo, press secretary of La Bancaria, a union representing workers in the financial sector. “We do not want to oppose the advance of technology, but we want technology to help rather than to replace or reduce jobs.”

Pesce was tapped to head the Central Bank by President Alberto Fernández, who has long expressed support for labour unions. With Argentina’s general election scheduled for October, the Central Bank’s position on authorising branch closures could change under a new administration.

Not all Argentine banks are contending with the problem of ghost branches. Some are smaller companies with fewer locations. Others, like Banco Macro, have a bigger presence in rural areas in the country’s interior, where in-person banking is more common.

But for most of Argentina’s banks, spending on empty branches is rising just as revenues fall amid economic weakness and government limits on lending rates. Large banks had efficiency ratios — a key metric to assess profitability — of 70 percent to 80 percent, compared with 50 percent for peers elsewhere in South America. A lower ratio indicates better performance. Argentine bank stocks also lagged Latin American rivals last year.

Vacant branches also make mergers and acquisitions difficult, because buying a bank in Argentina means taking on the cost of maintaining the unused sites.

“Branch closures are a global trend, due to digitalisation and because the costs of maintaining these and the employees are relevant. But the process of closing a branch is very complex in Argentina,” said Marcelo de Gruttola, a senior analyst for Latin America at Moody’s.

In the meantime, Argentine banks, like others around the world, are reimagining how to use real estate. Ideas under consideration include transforming the branches into cafés, training rooms for employees or places to pick up deliveries from e-commerce sites. In some cases, the banks keep a few desks available so customers can use the computers.

“Luckily, we don’t see many branch closures,” said Bustelo, the union representative. “We only see their digitalisation.”

by Ignacio Olivera Doll, Bloomberg

Comments