For all its political woes and still-stale economy, Brazil is standing out to investors as an unlikely island of stability as trouble brews across Latin America.

Money managers from Pacific Investment Management Co. and BlackRock Inc. are among those bullish on the nation’s assets. The main reason is the extensive reform agenda of the government, which after successfully overhauling a burdensome pension system now plans to tackle everything from a notoriously complicated tax system to a bloated state structure. The central bank has added to the optimism by slashing interest rates to a record as inflation runs below the target.

It’s a very different picture elsewhere in the region, which has been engulfed by growing political turmoil. Over the past few weeks, Chile and Ecuador declared states of emergency amid violent protests, Argentina tightened capital controls after the election of Alberto Fernández, Peru’s President shut the congress, and clashes erupted in Bolivia after Evo Morales was elected for a fourth term as president.

Upbeat mood

“Brazil is certainly standing out,” said Axel Christensen, the chief strategist for Latin America at BlackRock in New York. The prospect of tax, federal and administrative reforms, combined with low rates, are all boosting investor appetite for the country, he said.

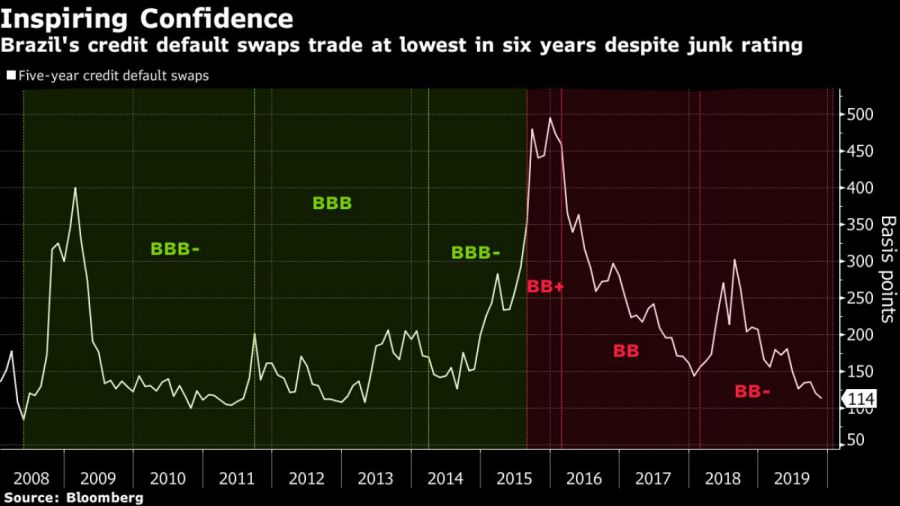

The upbeat mood is clear in asset moves, which have mostly shrugged off the infighting in the ruling party and controversies surrounding President Jair Bolsonaro. The Brazilian real was the best performer in the region last month and stocks are trading at an all-time high. The main exchange-traded fund dedicated to the country’s stocks, the US$9.4 billion iShares MSCI Brazil ETF, just had its biggest monthly inflow this year, and country’s risk as measured by five-year credit default swaps is at the lowest level since 2013 -- a time when Brazil’s debt was still rated investment grade.

“While Brazil is no stranger to political turmoil, its political class has started to understand the need to shield the economic agenda from political noise,” said Ismael Orenstein, a money manager at Pimco in Newport Beach who’s overweight Brazil’s local assets. “We are also starting to see some green shoots on the activity and credit side that make us more positive on the outlook for economic growth and assets such as the currency and corporate credit.”

This week, Brazil’s government announced a series of economic measures, with officials outlining plans to halt minimum wage increases, decentralize the budget and resume privatization of the utility Eletrobras. The country is also holding what may be the world’s priciest-ever sale of oil prospects.

After years of growth disappointments, some analysts are becoming more bullish on Brazil’s economy, saying 2020 is the year the country will finally deliver a positive surprise. They are betting record low borrowing costs will boost lending and consumer spending, and the conclusion of the pension reform after years of debate will give foreign investors more confidence to put money in the country.

Reform agenda progress

Progress in the reform agenda, low inflation and monetary easing are already lifting confidence levels and this could indicate a sustained recovery in economic activity, Bank of America Merrill Lynch economists led by David Beker wrote in a Wednesday report. They recently revised up their growth forecast for next year to 2.4 percent from 1.9 percent, above the market median of 2 percent.

“Getting pension reform passed is going to be big in the short and long term, and the government still seems serious and optimistic about plans to privatize more assets,” said Brendan McKenna, a currency strategist at Wells Fargo Securities LLC in New York.

His optimism doesn’t spread to all the rest of the region. McKenna says he has become more worried about Chile, as the cancellation of the Apec Summit in Santiago “admits some type of defeat,” while Argentina is “still a mess.” He’s more bullish on Colombia, where he says the economy is doing relatively well and inflation is low and somewhat stable.

In Mexico, meanwhile, bearish views are mounting. Morgan Stanley on Wednesday recommended taking profit in the country’s assets as the risk of a fiscal slippage, unlikelihood of a growth pick up, heavy positioning and stretched valuations mean the returns are no longer compensating the risk. They said at current prices they prefer to hold Brazil’s sovereign bonds over Mexico’s, especially in the 10 to 30 year space.

“Brazilian assets have further upside, mainly due to the impact of lower rates, privatization and micro economic reforms,” said Gustavo Medeiros, the deputy head of research at Ashmore Group Plc in London. “It won’t be a straight line, but the case for a sustainable rebound on earnings and subsequently investment and GDP growth is there.”

Comments