It is becoming increasingly difficult to read through the thick layer of uncertainty that hangs over Argentina’s socio-political ecosystem. More so than usual, in great part due to the combined effects of a tumultuous electoral process and pervasive economic stagflation that is extremely palpable to the population given triple-digit inflation. At the same time, Argentine stocks have gone on an incredible rally that promises to continue, dragging along rising valuations in the beleaguered sovereign bond sector as a shift in investor sentiment points to change in the political class’ relationship with the market. This isn’t a new trend as the collective group of economic agents we call “the market” has made very clear in the recent historical period, showing huge pessimism the greater the power of Cristina Fernández de Kirchner and massive optimism when it sees the “market-friendlies” making a comeback. Yet, the situation in the streets promises to be challenging, as recent events in the northern province of Jujuy have indicated, foreshadowing a complex scenario in the months and years ahead, especially if a reform-minded government makes it to the Casa Rosada and sticks to its promises.

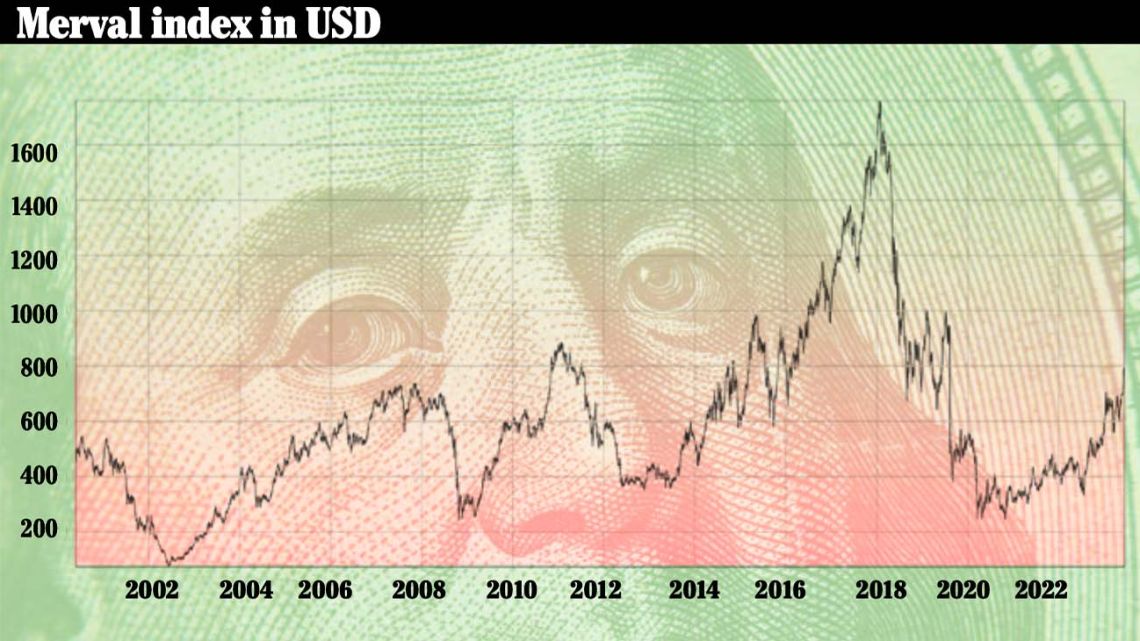

In the multiverse that is Argentina, it is the best of times and it is the worst of times, to paraphrase Dickens. From a financial standpoint, Argentina is back in the game. While for years it was considered a global financial pariah, and to a certain extent it still is, investors have sensed opportunity in a country with interesting prospects and massively undervalued assets. Businessmen and investors with international exposure are sensing that what was generally a conversation killer has now become a point of interest. “What can we buy?” they’re asked. Their bullish sentiment can be reflected in the value of Argentine stocks taken in US dollar terms, with the Merval index having gained nearly 40 percent thus far in 2023 despite clear signs that the economy is running out of steam given the chronic lack of foreign reserves. Sovereign bonds are also looking attractive to the point where financial powerhouse Morgan Stanley has recommended Argentina’s “junk bonds,” along with those from Ghana, Ukraine, Zambia, and El Salvador.

This appears contradictory when put in the context of Argentina’s macroeconomic situation, with the latest inflation reading coming in at 7.8 percent on a monthly basis and 114.2 percent year-on-year, and what appear to be signs of a stagnation in terms of output at least, if not an all-out contraction. One of the defining factors here is the (in)famous “electoral rally.” The current surge in the value of Argentine stocks is intimately tied with a repositioning of portfolios ahead of what the market expects to be a change in the country’s political leadership. Something similar occurred in 2014 when market participants sensed an exhaustion of the Kirchnerite model that had been in power for more than a decade. Shares rallied through the election where Mauricio Macri narrowly beat Daniel Scioli and the gains continued all the way through the first two years of the Cambiemos administration, generating returns to the tune of 350 percent. But Macri’s model quickly crumbled as 2018 came along, causing the deepest destruction in asset values at least in the past two decades as shares fell over 740 percent through to 2020, when Alberto Fernández took office with Fernández de Kirchner as his vice-president.

Going back to the 2001-2002 implosion of the Argentine economy, markets initially liked the Kirchner clan, with Néstor taking over in 2003 and leading a powerful comeback alongside then-economy minister Roberto Lavagna that saw stocks rally nearly 800 percent through to late 2007. That’s when the Cristina-Julio Cobos tandem took over, having won 45 percent of the vote. Immediately after things got complicated for CFK, as the subprime mortgage crisis in the US spread like the coronavirus to infect the global economy, also putting an end to the commodities supercycle fed by Chinese demand that allowed Argentina to keep dual surpluses for nearly a decade. A 61-percent decline in the value of Argentine stocks ensued over the coming year. From the 2009 bottom, the Merval surged to new heights, peaking as it came into 2011 with a 230 percent rally that would all but disappear as the electoral season came around and CFK, this time with Amado Boudou as her running-mate, took the election with 54 percent. Stocks tanked once again, this time falling 54.5 percent until the “Macri-electoral rally” mentioned above.

The wild ride in the value of Argentine assets is deeply impacted by exogenous factors, particularly international financial conditions. It is also closely connected to the political cycle, particularly the dichotomy between Fernández de Kirchner’s brand of Peronism and the supposedly market-friendly opposition, incarnated in the figure of Mauricio Macri over the past decade but moving beyond him this electoral cycle. According to economist Guido Lorenzo, it’s about moderation and extremes this time around. Whether the victor responds to Juntos por el Cambio or Unidos por la Patria, market participants will value a moderate political stance and an orthodox policy plan based on structural reforms and an inflation stability plan. If a candidate closer to Fernández de Kirchner or Javier Milei were to emerge from the PASO primaries with clear chances going into the general election, then the market may begin to have cold feet. Lorenzo doesn’t see the International Monetary Fund pushing Argentina into default despite having failed to comply with the targets set in its structural programme, which should allow the country to make it the handover in which Alberto Fernández’s successor is sworn in. Future prospects for the country are reasonably good given a favourable international situation, ample natural resource supply and an economy that could be standing on its feet relatively quickly. It’s not expensive to jumpstart the Argentine economy, the issue is trust.

The question, then, turns to politics. Is it possible to push through a consensus-driven reform programme in Argentina? One of the defining moments of the Macri administration was its (unilateral) decision to pass a provisional reform in late 2017 after winning the midterm elections, leading to a bloody street battle with combative sectors of the opposition that included both Kirchnerites and the traditional left. During the Fernández-Fernández administration, economy ministers Martín Guzmán and Sergio Massa suggested the implementation of stability plans that were quickly blocked by Máximo Kirchner and members of La Cámpora political organisation. In deeply polarised Jujuy, where Governor Gerardo Morales is one of Juntos por el Cambio's key players, political violence returned as constitutional reform was being passed with support of the local Peronist party. Beyond the merits or flaws of those reforms, there appears to have been a clear decision to confront him violently, and Morales didn’t hold back, unleashing the security forces.

The market’s expectation going into the electoral season is that moderates will take the presidency. If that prediction were correct, then the next government would seek to organise the macroeconomic situation using a relatively orthodox economic recipe, which will unquestionably generate social and political unrest. If this is how it plays out, the coming administration’s capacity to resist and govern through crisis will determine whether it succeeds in putting the country on a sustainable path going into the future. The conditions, however, are there.

Comments