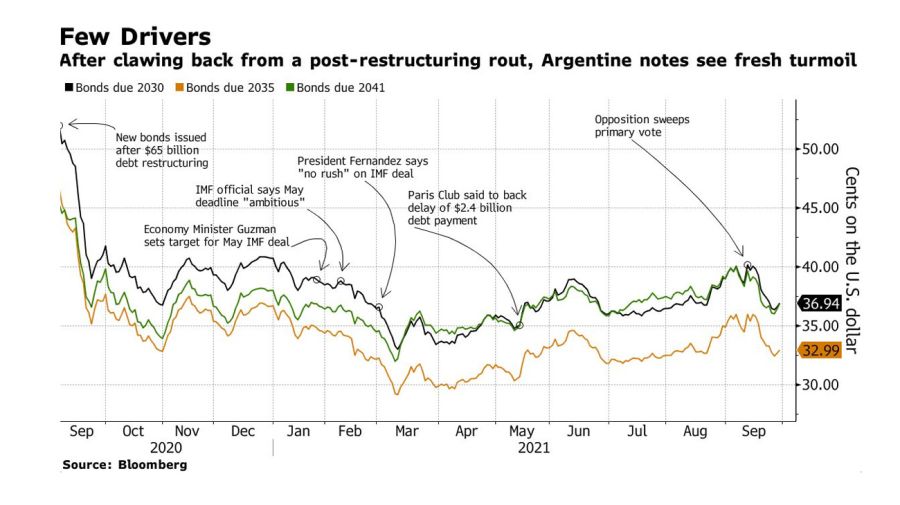

Argentina’s primary election went just the way investors wanted, delivering a stinging rebuke to President Alberto Fernández and leftist policies that have upended the economy.

It was exactly what traders who had bid up sovereign notes to a nine-month high before the vote were envisioning – a drubbing so severe that certainly it would lead Fernández to finally put aside the failed policies of Argentina’s radicals and turn toward economic orthodoxy for the last two years of his administration.

Instead, he seems to be going in the opposite direction.

Soon after the loss two weeks ago, Fernández remade his Cabinet by replacing some of the more moderate members. He promised to ramp up social spending ahead of the November vote that will decide control of both houses of Congress. And he has sped up money printing to pay for it all, a move that risks worsening inflation already running at 50 percent.

Bonds have taken a nose dive as Fernández goes all in on economic populism, posting one of the world’s worst performances since the vote and handing investors losses of more than three percent. Prices recently tumbled to about 30-some cents on the dollar, their lowest since July, over concern the surge in spending will further damage Argentina’s already precarious finances, undermine the currency and eventually lead to another multi-billion-dollar default, the country’s fourth this century.

Further adding to market pessimism is the lack of events on the horizon that could provide some relief before general elections in 2023. A deal to rework Argentina’s US$45-billion credit with the International Monetary Fund would have once been a positive development. But negotiations will be complicated by Fernandez’s insistence on populist spending, which will empty Argentina’s already dangerously low liquid reserves by year-end, according to Mauro Roca, managing director of emerging markets at TCW Group Inc. in Los Angeles.

“Alberto Fernández’s administration is practically betting the house on the midterm elections,” said Roca, who oversees US$17 billion in emerging-market assets. “There’s going to be payback for those policies in the form of inflation, and the IMF talks will be taking place under even worse conditions than we’re seeing now.”

Investors have grown disillusioned by the eternal promise of moderation from Fernández’s government, futilely waiting for an unwinding of capital controls, the lifting of export restrictions and an end to the price fixing Argentina has used to manage the economy. Hopes were further dashed by post-election comments from Vice-President Cristina Fernández de Kirchner in which she blamed the president’s economic strategy for a “political catastrophe.” Now more than ever, Fernández’s fractured ruling coalition is unlikely to agree on methods to return the country to growth, according to Diego Ferro, founder of M2M Capital in New York.

“You’re not going to see coherent economic policies out of a government run by groups of people who have very different views on the direction and identity of the country,” Ferro said. “In two years, it’s hard to know what kind of Argentina the next government is going to inherit.”

Fernández’s allies suffered at the polls amid political scandals over flaunting quarantine rules and early access to coronavirus vaccines, as well as a perceived mismanagement of the pandemic response. The opposition Juntos por el Cambio coalition took most of the country’s districts, including an unexpected victory in Buenos Aires Province, which accounts for more than a third of the total electorate.

That’s not to say it’s all bad news for Argentines. With almost half the population fully vaccinated against Covid-19 and a relaxation of pandemic restrictions ahead of the summer tourist season, the economy is expected to rebound almost seven percent this year, according to forecasts compiled by Bloomberg. Gross domestic product contracted 10 percent last year as the nation suffered through one of the world’s most prolonged lockdowns.

The best bet for investors in Argentina may be shifting into recently restructured bonds from Buenos Aires Province, which carry higher coupons than Argentina’s notes, according to Siobhan Morden, the head of Latin America fixed income at Amherst Pierpont in New York.

Buenos Aires-based brokerage Portfolio Personal Inversiones suggests taking a defensive posture, ditching Argentina’s most recently issued bonds for older securities that sport slightly higher coupons and stronger legal protections for investors.

Walter Stoeppelwerth, a fund manager at Gletir Corredor de Bolsa, said Argentina’s fiscal situation makes it inevitable that a reckoning lies ahead.

“The numbers don’t lie,” he said in a webinar hosted by Portfolio Personal Inversiones on Thursday. “The biggest risk to being a bondholder in Argentina is that the government runs out of dollars again.”

related news

by Scott Squires, Bloomberg

Comments