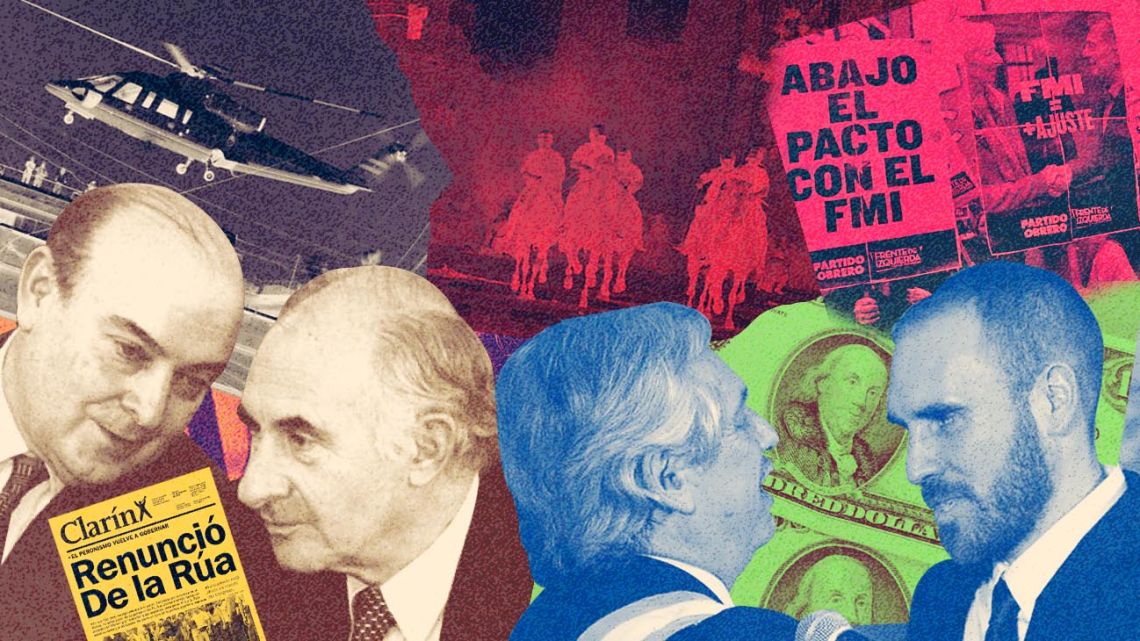

Twenty years have passed since Argentina imploded in what was its worst social and political crisis, at least in modern times. The beleaguered nation defaulted on a US$96-billion loan, failing to gain support from the United States and the International Monetary Fund and watching five presidents come and go from the Casa Rosada in a period of two weeks until Eduardo Duhalde, a Peronist who had been defeated in general elections a few years earlier by the freshly resigned Fernando De La Rúa, took over, paving the way for more than a decade of Kirchnerismo.

Fast forward to today and Argentina’s massive debt pile is still front and centre of the political discussion, as is the IMF and the possibility of default. There can be little doubt that the 2001 crisis marked a schism in Argentine history, and that Alberto Fernández, Mauricio Macri and Cristina Fernández de Kirchner all gained their centrality in today’s political arena as a consequence of the shockwaves still reverberating through the system. While that much is clear, it isn’t easy to imagine that Argentina and the IMF have truly learned their lessons and will be able to build a constructive relationship that will help the country find its way out of nearly a century of economic mediocrity.

When speaking of economic mismanagement, Argentina holds several world records. We’ve defaulted on our sovereign debt nine times, starting back in 1827, when the nation was in diapers. We held the record for the largest-ever sovereign default in history at US$96 billion in 2001. Argentina firmly holds on to its place among the world’s top countries for yearly price increases, with inflation hitting an annualised 52.1 percent in the latest report from INDEC national statistics bureau. With 21 IMF agreements since 1958, we received the largest-ever bailout at US$57-billion in 2018 and remain its largest debtor, with US$44-billion of that mega credit-line disbursed.

The situation in 2001 was drastically different from today. After the hyperinflations of the late 1980s, in the aftermath of the 1976-83 military dictatorship, president Raúl Alfonsín was unable to tame the economy, forced to resign before the end of his term and paving the way for Carlos Menem, the neoliberal Peronist, to take office. Following the economic fashion of the times, Menem and economy minister Domingo Cavallo followed the Washington Consensus, pursuing a pro-market policy of deregulation and privatisation, while implementing a currency board known as the Convertibility Plan which fixed the value of the dollar at one peso. It worked wonders in taming inflation and spurring economic growth, making Argentina the emerging market darling and allowing it to borrow cheaply – and recklessly – in foreign currency. By 1998 economic momentum had slowed, Argentina fell into recession, the sovereign and the provinces had racked up large deficits, unemployment was on the rise, and convertibility had become an addiction. As De La Rúa, a member of the Civic Radical Union (UCR), took office he vowed to cut the deficit and end corruption, but found himself in bed with the IMF as the economy dismantled before his eyes. Unable to end convertibility, he called Menem’s economy minister, Cavallo, to his aid. The second the IMF cut its emergency funding, the economy collapsed, the nation defaulted, and the hard peg between the peso and the dollar ended.

Néstor Kirchner was Duhalde’s protégé, taking power in 2003 and eventually ridding himself of his old master. Kirchner led the country through one of its strongest periods of economic growth as he surfed the commodities super-cycle, expanding the use of social plans in order to ameliorate the impact of the loss of formal employment in the aftermath of the 2001 implosion (something similar happened in Brazil). At the same time, Néstor began a tough debt restructuring battle with creditors, strengthened by dual surpluses on the back of rising commodity prices.

The global financial crisis sparked by the subprime bubble marked the end of the super-cycle fuelled by Chinese growth, and Argentina, now governed by Cristina Fernández de Kirchner, saw its model run out of gas. Rather than relying on reforms to improve the competitiveness of the Argentine economy, Cristina and her economic team, led by the likes of Amado Boudou and Axel Kicillof, relied on sacking pension plans, the state energy company (YPF), and every which coffer they could find. Deficit spending, inflation, export taxes, currency controls and dual exchange rates on the one hand, with incendiary rhetoric, all-out war against its opponents, and la grieta (polarisation) on the other.

One of the good things about being locked out of international debt markets for the Kirchnerites was that they handed over a state that wasn’t heavily indebted in foreign currency, but Cristina’s administration did see a large surge in intra-government debt. She left Macri a ticking time bomb when he took office, with a lack of foreign exchange reserves that led to hard currency controls and intense pressure on the official exchange rate. A massive fiscal deficit and manipulated official statistics agency meanwhile masked inflation and unemployment.

Macri and his team quickly deactivated that bomb by lifting the cepo and closing a deal with holdout creditors and “vulture funds” like Paul Singer’s Elliott Management. Yet the Cambiemos leader was unable to effectively tackle deficit spending, which he actually increased initially. Inflation was never under control and relying on sovereign debt in US dollars led to several runs on the peso at the first sign of danger, as when Turkey (it’s always Turkey) suffered a currency crisis in 2018. Not only did Macri grow the deficit and take on a boatload of dollar-denominated debt, he never managed to use his political capital to pass much needed and promised reforms. He finished as he started, with another cepo and handing over a ticking time bomb to his successors, the Fernández-Fernández tandem.

Alberto and Cristina received an imploded economy and had to face the global coronavirus pandemic. But, as mentioned in previous columns, there’s no more time for excuses, with an impossible debt calendar in the first quarter of 2022 ahead of us, inflation above 50 percent, poverty around 40 percent and a socio-economic situation that is every day closer to a breaking point.

Comments