A flare-up in exchange rate markets has sounded the alarm bells in Javier Milei’s Argentina for the first time, generating some sort of panic in the immediate aftermath of the long-awaited congressional approval of the ‘Ley de Bases’ and the accompanying fiscal package. With the government ready to take a victory lap, its top economic policy makers – Economy Minister Luis ‘Toto’ Caputo and his business associate installed at the Central Bank, Santiago Bausili – spooked market actors who were already jittery, accelerating a run on the peso reminiscent of the worst days of the Sergio Massa tenure.

It isn’t entirely clear why this administration, praised for its modern communications strategy in the hands of star advisor and spin doctor Santiago Caputo, suffered such an unforced error, with many recalling the ill-fated press conference held on December 28, 2017, when then-Central Bank governor Federico Sturzenegger was publicly humiliated by Cabinet Chief Marcos Peña while flanked by ministers Nicolás Dujovne (Economy) and Luis Caputo (Finance), marking the beginning of the end of the “pax macrista.”

Argentine society was beginning to get comfortable with an atmosphere of falling inflation and relative stability of the peso-dollar exchange rate, despite the continued warnings of established economists, many of them ideologically close to the president. Thus, while Milei and his libertarian ragtag team of misfits have taken up arms against a sea of political adversaries, gaining enemies both domestic and abroad, they have retained the steadfast support of a majority, along the lines of the run-off vote where La Libertad Avanza took home 56 percent. With the final approval of the Mileis sweeping reform package after six months in the legislative doldrums, it seemed like this administration would finally be able to count on the tools to get governing, fixing the underlying structural issues of the Argentine macroeconomy. The blue chip peso-dollar exchange rate, Argentina’s fear gauge, was expected to slide, in a sign of increased confidence in the sustainability of Milei’s policy plan, which should lead to a further strengthening of the value of Argentine bonds and therefore a lowering of the country risk-premium.

Instead, the opposite happened. And it had a very real and negative effect on the purchasing power of the population. Caputo and Bausili called a late-Friday-evening press conference the previous week then faced the banking sector again early this week, yet they failed to offer a credible policy path and timetable. If the doubts regarding Milei’s capacity to preside over Argentina were tied to governability risk, Caputo’s are connected to credibility risk: it’s difficult to see how the current policy framework can be sustainable in time. At the centre of it all is the exchange rate policy, where the official peso-dollar rate is allowed to slide along a “crawling peg,” meaning the rate of devaluation runs at two-percent monthly. A substantial devaluation in the early days of the administration gave Milei and Caputo a cushion on exchange rate markets, as inflation runs well above the crawling peg and progressively erodes the competitiveness of the exchange rate regime. In just a few months, Argentina went from extremely cheap in dollar terms to relatively expensive, while inflation did drop strongly on the back of a solid “fiscal anchor” or budget surplus and an engineered recession. As did the exchange rate premium, allowing the Central Bank to amass reserves.

That model seems to run out of steam, both local economists and the International Monetary Fund agree, leading to an inevitable barrage of insults from the President. The main recipient of his rage was Rodrigo Valdés, a prestigious Chilean economist who is running the IMF’s Western Hemisphere department. The man in charge of negotiating the future of Argentina’s relationship with the international lender of last resort is pushing the Milei-Caputo tandem to accept a devaluation and “unwind distortive taxes” in order to pave the way for a lifting of strict currency controls (“cepo”), in the same line as the agro-exporting sector which is sitting on grain, affecting the Central Bank’s capacity to fill up its coffers with hard currency reserves. According to one of the most influential provincial governors, the Milei administration promised it would reduce the PAIS tax, export taxes, and lift the “cepo,” promises that it hasn’t kept, leading the agro-exporting sector to adopt a “wait and see” strategy.

Milei and Caputo don’t appear willing to negotiate their economic plan in the same way as they ended up accepting amendments to their ‘Ley de Bases’ and fiscal package. Their intransigence will be put to the test by the International Monetary Fund, which essentially told the ultra-libertarian that he must forget his plans to torch the Central Bank and dollarise the Argentine economy. It seems as if Caputo was already leading Milei in that direction. Yet, the real question as to their dexterity to captain the ship over rough seas is now front and centre. As explained by economist Diego Giacomini, an anarcho-capitalist and former friend of the president, the Argentine government’s hard currency obligations throughout Milei’s tenure are impossible to honour, meaning that he will need to come up with fresh funds to a substantial degree while renegotiating debt. Will Milei, with his confrontational style, be able to sit down and iron out this level of agreement?

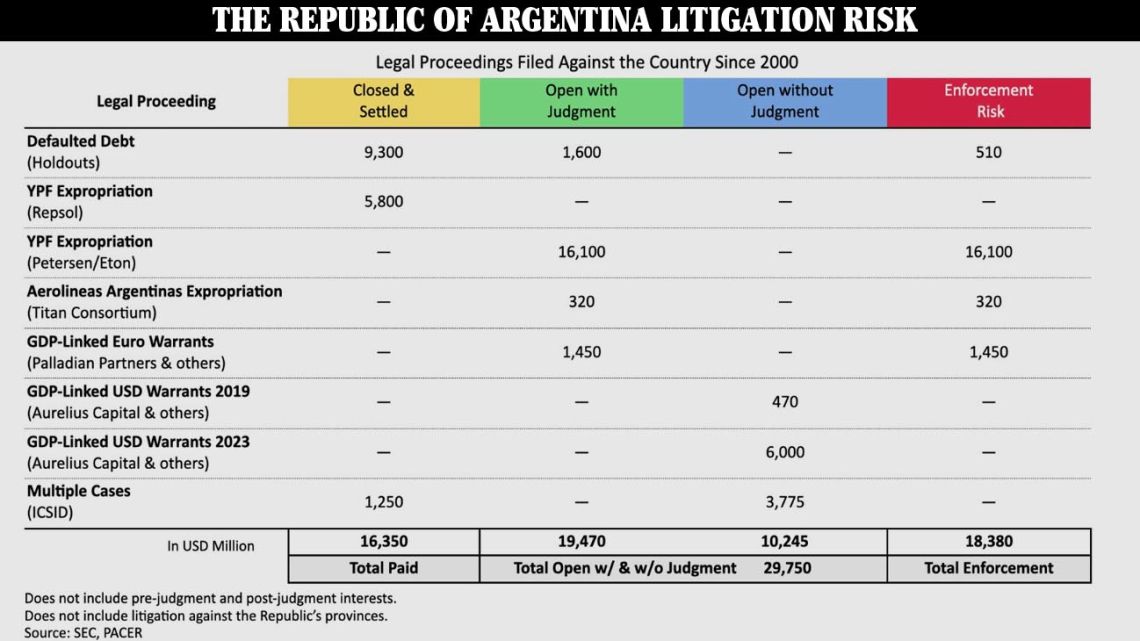

One example is the historic court case regarding the nationalisation of YPF that is currently underway in New York, where Judge Loretta Preska has ruled against Argentina, putting a US$16-billion price tag on the damages. According to Sebastián Maril, director of Latam Advisors and one of the foremost experts in Argentina’s foreign judicial issues, the sovereign state has already shelled out US$16.35 billion in closed and settled legal judgements since 2000, has another US$19.47 billion in litigation open with judgement (including the YPF case), and US$10.245 billion more open without judgement. These are cases tied to defaulted debts (holdouts), the expropriations of YPF and Aerolíneas Argentinas, GDP-linked warrants, and others. Given the government’s legal strategy of dragging out cases, it is on the verge of being ordered to hand over assets, including possibly its 51-percent stake in the state energy firm, which would lead to all sorts of complexities, including having to pass it through Congress.

The majority of these asset seizures are expected to occur during the Milei administration. “In 2024, Argentina should start viewing international legal proceedings as assets and not liabilities,” explained Maril. “Beneficiaries of foreign judgments should understand that, by helping the Republic they’ll be helping themselves.” In a livestream for Perfil’s digital subscribers, he noted that Burford Capital, the leading litigation fund involved in the YPF case, is not a vulture fund like Paul Singer’s Elliott Management. They could be easily persuaded to negotiate a deal that is worth substantially less than the US$16-billion judgement, paid over a longer period of time, while even bringing in much-needed foreign direct investment for Argentina.

Is Milei ready to begin to think outside the box, as he did electorally, and adopt a pragmatist’s playbook in order to receive much needed support from the outside world? Or will he retain a capricious attitude, stubbornly pushing forth with his plan until it either works or implodes? How long will the population, and the markets, give him time and space to operate? All of these questions are currently on the table, and for the first time in his Presidency he is under pressure.

Comments